If you’re considering retirement within the next five years or so, you’re in the retirement “zone.” This is a critical time period during which you’ll be faced with a number of important choices, and the decisions you make can have long-lasting consequences. It’s a period of transition: a shift from a mindset that’s focused on accumulating assets for retirement to one that’s focused on distributing wealth and drawing down resources. It can be confusing and chaotic, but it doesn’t have to be. The key is to understand the underlying issues, and to recognize the long-term effects of the decisions you make today.

Tip: If you’ve recently retired, you’re also in the retirement zone. You’ll want to evaluate your financial situation in light of the decisions that you’ve already made, and consider adjusting your overall plan to reflect your current expectations and circumstances.

Are you ready to retire?

The first question that you should ask yourself is: “Am I ready to retire?” For many, the question isn’t as easy to answer as it might seem. That’s because it needs to be considered on two levels. The first, and probably the most obvious, is the financial side. Can you afford to retire? More specifically, can you afford the retirement you want? On another level, though, the question relates to the emotional issues surrounding retirement–how prepared are you for this new phase of your life? Consider both the financial and emotional aspects of retirement carefully; retiring before you’re ready can put a strain on the best-devised retirement plan.

Tip: There’s not always a “right” time to retire. There can be, though, a wrong time to retire. If you’re not emotionally ready to retire, it may not make sense to do so simply because you’ve reached age 62 (or 65, or 70). In fact, postponing retirement can pay dividends on the financial side of the equation. Similarly, if you’re emotionally ready to retire, but come up short financially, consider whether your plans for retirement are realistic. Evaluate how much of a difference postponing retirement could make, and then weigh your options.

Transitioning into retirement: Financial issues

Start with the basics:

- If you do not already have a projection of the annual income you’ll need in retirement, spend the time now to develop one. Factor in anticipated costs relating to basic needs, housing, health care, and long-term care. If you plan to travel in retirement, estimate a corresponding annual dollar amount. If you’re financially responsible for other family members, or plan to make monetary gifts, you’ll want to include these commitments in your calculations. Be as specific as you can. If it’s been more than a year since you’ve done this exercise, revisit your numbers. Consider and account for inflation.

- Estimate the income that you’ll be able to rely on from Social Security and any benefits from a traditional employer pension, and compare the result with your projected retirement income need. The difference may need to be funded through your personal savings.

- Take stock of your personal savings. Are your personal savings sufficient to provide you with the annual income that you’ll need?

- When will you retire? The age at which you retire can have an enormous impact on your overall retirement income situation, so you’ll want to make sure you’ve considered your decision from every angle. Why does the timing of your retirement make such a difference? The earlier you retire, the sooner you need to start drawing on your retirement savings. You’re also giving up what could be prime earning years, when you could be making substantial additions to your retirement savings. That combination, even for just a few years, can make a tremendous difference.

Other factors to consider:

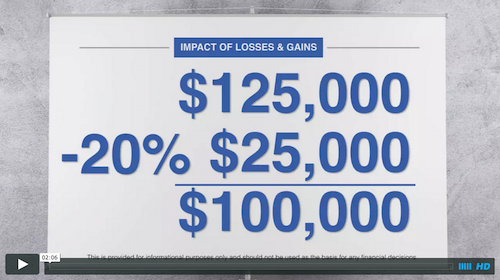

- The longer the retirement period that you need to plan for, the greater the potential that inflation will eat away at your purchasing power. That means the earlier you retire, the more important it is to account for inflation in your overall plan.

- You can begin receiving Social Security retirement benefits as early as age 62. However, your benefit may be as much as 20 to 30 percent less than if you waited until full retirement age (65 to 67, depending on the year you were born). Weigh your options, and choose the start date that makes the most sense for your individual financial circumstances.

- If you’re covered by a traditional employer pension plan, check to make sure it won’t be negatively affected by your early retirement. Because the greatest accrual of benefits generally occurs during the final years of employment, it’s possible that early retirement could effectively reduce the benefits you receive. Make sure that you understand how the plan calculates benefits and any payout options under the plan.

- If you plan to start using your 401(k) or traditional IRA savings before you turn 59½ (55 in the case of distributions from a 401(k) plan after you terminate employment), you may have to pay a 10 percent early distribution penalty tax in addition to any regular income taxes (with some exceptions, this includes payments made due to disability). Consider as well the order in which you’ll tap your personal savings during retirement. For example, you might consider withdrawing from tax-advantaged accounts like IRAs and 401(k)s last. If you postpone retirement beyond age 70½, you’ll need to begin taking required minimum distributions from any traditional IRAs and employer-sponsored retirement plans (other than your current employer’s retirement plan), even if you do not need the funds.

- You’re not eligible for Medicare until you turn 65. Unless you’ll be eligible for retiree health benefits through your employer (or have coverage through your spouse’s plan), or you take another job that offers health insurance, you’ll need to calculate the cost of paying for insurance or health care out-of-pocket, at least until you can receive Medicare coverage.

Transitioning into retirement: Non-financial issues

When it comes to retirement, it’s easy to focus on the financial aspects of your decision to the exclusion of all other issues. After all, we’ve spent much of our lives saving for retirement, and for many of us, the retirement lifestyle we hope to enjoy depends primarily on the wealth that we’ve accumulated during our working years. But, there are a number of non-financial issues and concerns that are just as important.

Fundamentally, your retirement income plan is just a means to an end: having the ability to do the things you want to do in retirement, for as long as you want to do them.

But that presupposes that you know what it is you want to do in retirement. Many of us have never thought beyond the vague notion we’ve held during most of our working lives: that retirement–if properly planned for–will be something of an extended vacation, a reward for a lifetime of hard work. Retirement may be just that … for the first few weeks or months. The fact is, though, that your job likely demanded your attention for a majority of your waking hours. No longer having that job leaves you with a lot of free time to fill. Just as you have a financial plan when it comes to your retirement, you should consider the type of lifestyle you want and expect from retirement as well.

What do you want to do in retirement? Do you intend to travel? Pursue a hobby? Give some real thought to how you’re going to spend a typical week, and consider actually writing down a hypothetical schedule. If you haven’t already, consider:

- Volunteering your time–You can provide a valuable service to the community, while sharing your unique skills and interests. Hospitals, community centers, day-care centers, and tutoring programs are just a few of the places where you could make a difference.

- Going to school–Retirement can be the perfect time to pursue a degree, advance your knowledge in your current field or in a new field, or just take classes that interest you. In fact, many institutions offer special rates and programs for retirees.

- Starting a new career or business–Retirement can be the perfect opportunity to try something different. If you’ve ever dreamed of starting your own business, now may be your chance.

Having concrete plans can also help overcome problems commonly experienced by those who transition into retirement without thinking ahead:

- Loss of identity–Many people identify themselves by their professions. Affirmation and self-worth may have come from the success that you’ve had in your career, and giving up that career can be disconcerting on a number of levels.

- Loss of structure–Your job provides a certain structure to your life. You may also have work relationships that are important to you. Without something to fill the void, you may find yourself needing to address unmet emotional needs.

- Fear of mortality–Rather than a “new beginning,” some see the “beginning of the end.” This can be exacerbated by the mental shift that accompanies the transition from accumulating assets to drawing down wealth.

- Marital discord–If you’re married, consider whether your spouse is as ready as you are for you to retire. Does he or she share your ideas of how you want to spend your retirement? Many married couples find the first few years of retirement a period of rough transition. If you haven’t discussed your plans with your spouse, you should do so; think through what the repercussions will be–both positive and negative–on your roles and relationship.

Working in retirement

Many individuals choose to work in retirement for both financial and non-financial reasons. The obvious advantage of working during retirement is that you’ll be earning money and relying less on your retirement savings–leaving more to potentially grow for the future, and helping your savings last longer. But many retirees also work for personal fulfillment–to stay mentally and physically active, to enjoy the social benefits of working, or to try their hand at something new. If you are thinking of working during your retirement, you’ll want to make sure that you understand how your continued employment will affect other aspects of your retirement. For example:

- If you continue to work, will you have access to affordable health care through your employer? If so, this could be an incredibly valuable benefit.

- Will working in retirement allow you to delay receiving Social Security retirement benefits? If so, your annual benefit when you begin receiving benefits may be higher.

- If you’ll be receiving Social Security benefits while working, how will your work income affect the amount of Social Security benefits that you receive? Additional earnings can increase benefits in future years. However, for years before you reach full retirement age, $1 in benefits will generally be withheld for every $2 you earn over the annual earnings limit ($15,720 in 2015). Special rules apply in the year that you reach full retirement age.

Tip: Some employer pension plan programs allow for “phased retirement.” These programs allow you to continue to work on a part-time basis while accessing all or part of your pension benefit. Federal law encourages these phased retirement programs by allowing pension plans to start paying benefits once you reach age 62, even if you’re still working and haven’t yet reached the plan’s normal retirement age.

Caution: Many people who count on working in retirement find that health problems or job loss prevents them from doing so. When making your retirement plans, it may be wise to consider a fallback plan in case everything doesn’t go as you expect.

Important Disclosure

Are any life-changing events coming up soon, such as marriage, the birth of a child, retirement, or a career change?

Are any life-changing events coming up soon, such as marriage, the birth of a child, retirement, or a career change? You’ll want to check your withholding, especially if you owed taxes when you filed your most recent income tax return or you received a large refund. Doing that now, rather than waiting until the end of the year, may help you avoid a big tax bill or having too much of your money tied up with Uncle Sam. If necessary, adjust the amount of federal or state income tax withheld from your paycheck by filing a new Form W-4 with your employer.

You’ll want to check your withholding, especially if you owed taxes when you filed your most recent income tax return or you received a large refund. Doing that now, rather than waiting until the end of the year, may help you avoid a big tax bill or having too much of your money tied up with Uncle Sam. If necessary, adjust the amount of federal or state income tax withheld from your paycheck by filing a new Form W-4 with your employer.