As a retirement income planning company for women, we often get financial questions. We’ve written the top 5 FAQ for married women below in hopes that it could be of benefit to you as a woman. If you have a question of your own, feel free to let us know!

Am I liable for my spouse’s debts?

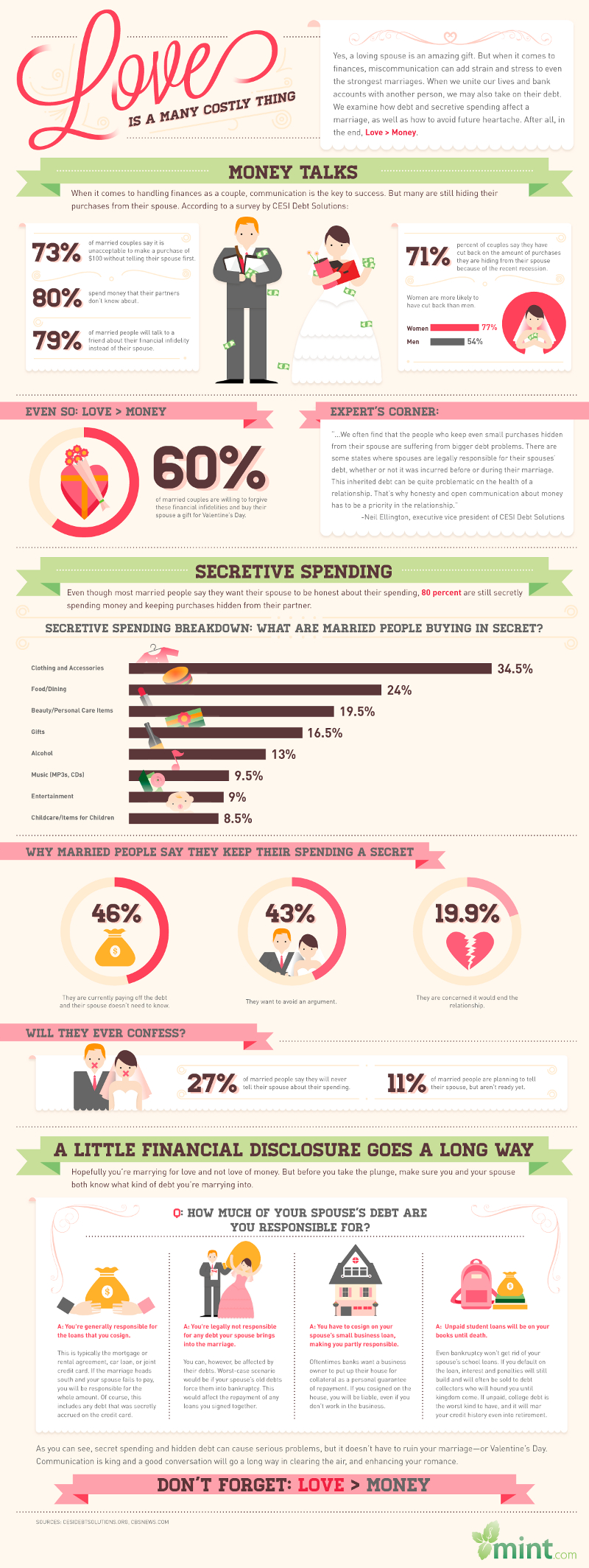

The general rule is that spouses are not responsible for each other’s debts, but there are exceptions. Many states will hold both spouses responsible for a debt incurred by one spouse if the debt constituted a family expense (e.g., child care or groceries). In addition, community property states will hold one spouse responsible for the other’s debts because both spouses have equal rights to each other’s income. Also, you are both responsible for any debt that you have in both names (e.g., mortgage, home equity loan, credit card).

I’m marrying someone with bad credit. How will this affect me?

You are not responsible for your future spouse’s bad credit or debt, unless you choose to take it on by getting a loan together to pay off the debt. However, your future spouse’s credit problems can prevent you from getting credit as a couple after you’re married. Even if you’ve had spotless credit, you may be turned down for credit cards or loans that you apply for together if your spouse has had serious problems.

You’re smart to face this issue now rather than wait until after you’re married to discuss it. Attitudes toward spending money, along with credit and debt problems, often lead to arguments that can strain a marriage. Order copies of both of your credit reports from one or more major credit reporting bureaus. Then, sit down and honestly discuss your past and future finances. Find out why your future spouse got into trouble with credit.

Next, if there is still outstanding debt, consider going through credit counseling together. Credit counseling may help your future spouse clean up his or her credit record and get back on track financially. Finally, seriously consider keeping your credit separate, at least until your spouse’s credit record improves. You don’t have to combine your credit when you marry. For instance, apply for credit by yourself instead of applying for joint credit after you’re married. You can have separate “associate” cards issued for your spouse to use. Even if your spouse has bad credit, your credit rating will remain unaffected. However, keeping separate credit can be complicated. For one thing, your spouse may resent that you control all of the credit in the household. It’s also possible that you’ll have a harder time qualifying for loans (e.g., a mortgage) alone than if your spouse’s income could also be counted.

I’m getting remarried. How will this affect my Social Security benefits?

If you’re receiving benefits based on your own work record, your benefits will continue. If you’re receiving spousal benefits based on your former spouse’s work record, those benefits will generally end upon your getting remarried, but you may be able to receive benefits based on your new spouse’s work record, or on your own.

If you’re a widow(er) under age 60, or you’re disabled but under 50, remarriage ends any benefits based on the record of your deceased spouse. However, if you remarry after age 60 (or after 50 and are disabled), those benefits remain intact, unless you get spousal benefits through your new spouse (at age 62 or older) if those benefits are higher. If your second marriage ends as a result of death, divorce, or annulment in less than 10 years, you will again be eligible to collect benefits on your first spouse’s record. Benefits paid to a disabled widow(er) are unaffected by remarriage.

Note, too, that if you were the working spouse during your first marriage, your remarriage does not change the Social Security benefits paid to either your new spouse or ex-spouse. Because the rules surrounding payment of benefits are complicated, and depend on your particular situation, contact the Social Security Administration for more information.

I don’t know much about investing. Should I let my husband make the decisions?

Even if your husband is a financial expert, it’s a good idea to at least understand investing basics. For one thing, because women on average tend to live longer than men, the odds are extremely high that you could be responsible for making your own financial decisions at some point. If you suddenly had to make all the decisions yourself–and many women have found themselves in that position–you’d benefit from knowing enough to protect yourself from fraud.

Also, even if your spouse is more knowledgeable about finances than you are, understanding enough to consider the pros and cons involved in an individual financial decision can often produce a better outcome; it forces both of you to address questions you might not have considered otherwise. Knowing why a decision was made can help minimize second-guessing on either side later.

If you disagree about a particular investment, remember that though diversification doesn’t guarantee a profit or prevent the possibility of loss, a diversified portfolio should have a place for both conservative and more aggressive investments. There may be ways to accommodate both spouses’ concerns, and a neutral third party with some expertise and a dispassionate view of the situation may be able to help you work through differences.

My spouse and I are filing separate returns. Can we both itemize our deductions? If so, how do we split the deductions?

When spouses file separately, both must use the same method of claiming deductions. That is, either both parties must itemize, or both parties must take the standard deduction. If you choose to itemize, it’s important to know how to divide your deductions.

If your filing status is married filing separately, you typically report on your income tax return only your own income, expenses, credits, and deductions. Therefore, if you paid for a doctor’s appointment out of your separate checking account, you would claim that deduction on your return. Any medical expenses paid out of a joint checking account in which you and your spouse have the same interest are considered to have been paid equally by each of you, unless you can show otherwise. Different rules may apply in community property states.

You should also be aware that the amount of your total itemized deductions will be limited or phased out if your adjusted gross income exceeds certain levels for years after 2012.

Often, married couples have a lower overall tax liability if they choose to file jointly. This is not always the case, however. If you are unsure which filing method results in the lowest tax liability, you should determine your tax liability both ways before filing your return.

For more information, see IRS Publication 17 or consult a tax professional.

— 2 Comments —

Comments are closed.